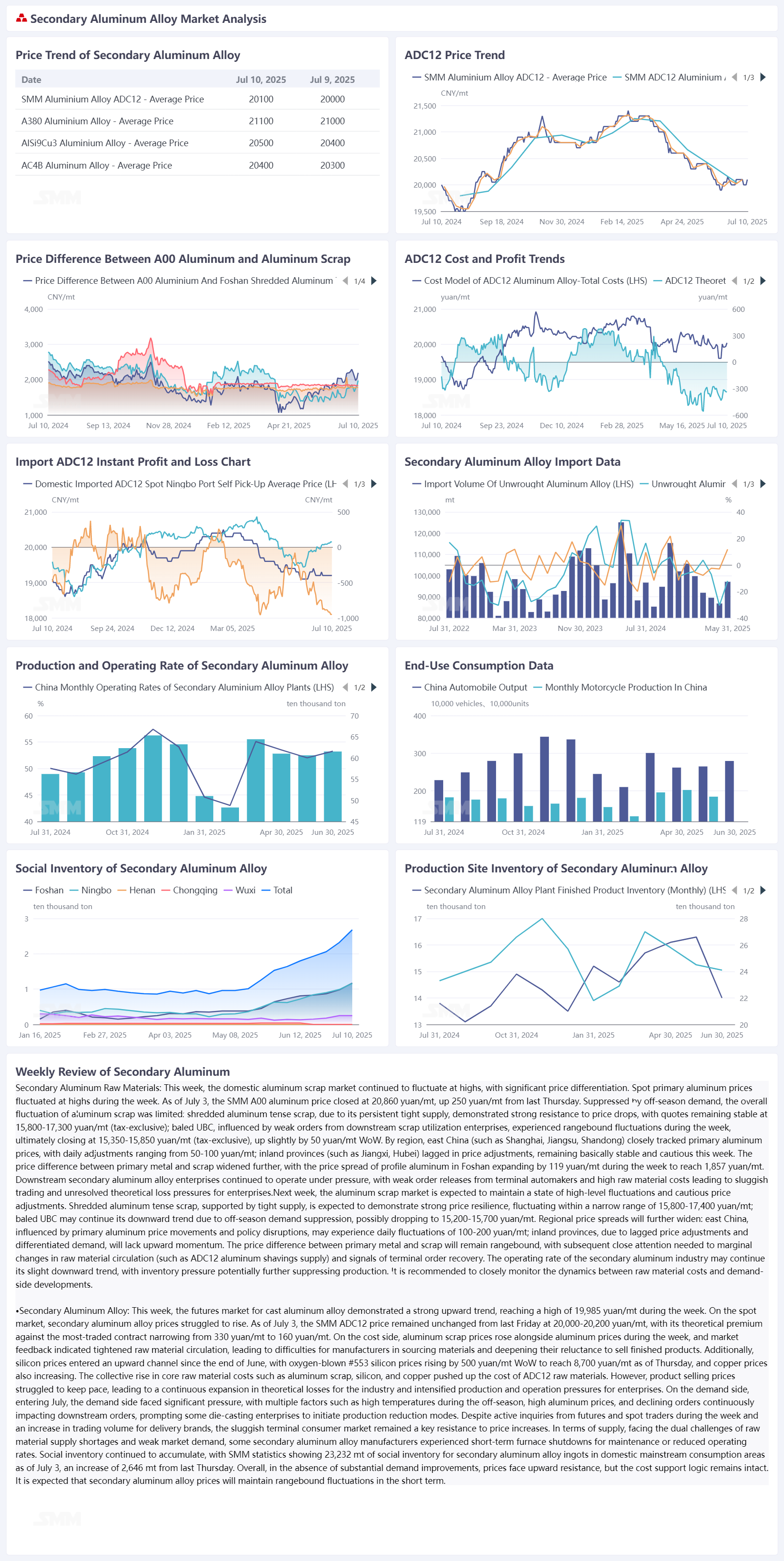

The domestic aluminum scrap market hovered at highs this week, with prices showing significant divergence. Spot primary aluminum prices fluctuated at highs during the week, with the SMM A00 price closing at 20,820 yuan/mt on July 10, down 40 yuan/mt WoW. Affected by weak orders from downstream scrap utilization enterprises and rigid procurement demand during the traditional off-season, the overall upside of aluminum scrap prices was limited. Among them, shredded aluminum tense scrap benefited from persistent tight supply, demonstrating notable price resilience, with weekly offers basically stable at 15,800-17,400 yuan/mt (ex-tax). Baled UBC prices fluctuated rangebound due to evident demand pressure, eventually settling at 15,350-15,850 yuan/mt (ex-tax).

Regional performance varied significantly: East China (Shanghai, Jiangsu, Shandong) closely tracked primary aluminum prices with frequent and sizable adjustments (50-150 yuan/mt), while Jiangxi, Guizhou, Hunan, and Guangdong lagged in price adjustments, mostly holding steady with only Jiangxi seeing a counter-trend hike. The price difference between primary metal and scrap further widened, with the spread for Foshan profile aluminum expanding to 1,975 yuan/mt during the week.

Next week, the aluminum scrap market is expected to maintain its high-volatility pattern, with continued divergence by product and region. Shredded aluminum tense scrap will remain strongly supported by tight supply, likely staying the most resilient within a narrow range of 15,800-17,400 yuan/mt. Baled UBC faces greater downward pressure due to weak off-season demand, potentially testing 15,200-15,700 yuan/mt. Regionally, east China may continue closely mirroring primary aluminum fluctuations, with daily adjustments possibly widening to 150-200 yuan/mt. Inland and southern provinces (e.g., Jiangxi, Hunan, Guizhou, Guangdong) may lack follow-through momentum due to delayed adjustments and local supply-demand dynamics, potentially further widening price spreads.

Cast aluminum alloy futures experienced a decline followed by a rebound this week. After extending the previous week's downtrend on Monday, they rebounded from Tuesday onwards, reaching a new listing high of 20,000 yuan/mt on Thursday. Spot prices exhibited a narrow rangebound fluctuation, first declining and then rising. As of July 10, the SMM ADC12 price was reported at 20,000-20,200 yuan/mt, unchanged from last Friday, with its theoretical premium against the most-traded contract narrowing to 145 yuan/mt. Cost support continued to strengthen during the week. Affected by reduced aluminum scrap imports and high temperatures suppressing dismantling volumes, domestic and overseas aluminum scrap supplies tightened, exacerbating the difficulty for secondary aluminum plants to procure raw materials. Intense competition for "material scrambling" in the market drove up production costs, thereby supporting ADC12 quotes. Weak demand constituted the core resistance to price increases. Although market expectations for H2 consumption turned optimistic, the high-temperature off-season in July continued to suppress the operating rates of downstream die-casting enterprises. Coupled with high aluminum prices eroding terminal purchase willingness, short-term demand was unlikely to improve. In terms of supply, differentiation persisted. Large plants, leveraging stable orders and the advantage of delivery brands, were expected to maintain stable or increase production, driven by futures and spot traders actively procuring ADC12 for futures-spot arbitrage. However, as the traditional off-season deepened, automakers might cut production due to high-temperature holidays and finished product inventory pressures. Additionally, raw material shortages and intensified cost pressures led some enterprises to halt furnaces for maintenance at the end of June or early July, which would drag down the industry's overall operating rate. Social inventory remained on an inventory buildup trajectory. According to SMM statistics, as of July 10, the social inventory of secondary aluminum alloy ingots in domestic mainstream consumption areas was 26,766 mt, an increase of 3,534 mt from last Thursday. Affected by typhoons, the shipment of aluminum alloy ingots in Ningbo and other places was hindered. It was expected that shipments would resume after the typhoon weather ended, and inventory would continue to increase next week.

Overall, the tug-of-war between strong cost support and weak demand suppression persisted, and it was expected that ADC12 prices would maintain a narrow rangebound fluctuation pattern in the short term.